For many families living on or near the poverty line, access to banking, credit and additional funds is challenging. To combat this, some financial institutions have established microfinance or micro-credit programs — small loans designed to assist traditionally underserved sections of society.

Unlike traditional charitable donations designed to immediately mitigate urgent requirements, microfinance is designed to provide support for long-term improvements to quality of life, health and education. Many families across the globe are either living in poverty or surviving on near subsistence level, which provides little additional income for cumulative improvements or reliable access to basic services. Microfinance seeks to bridge this gap without overly burdening the recipient with debt, by giving small loans to those who may otherwise be refused by traditional money lenders.

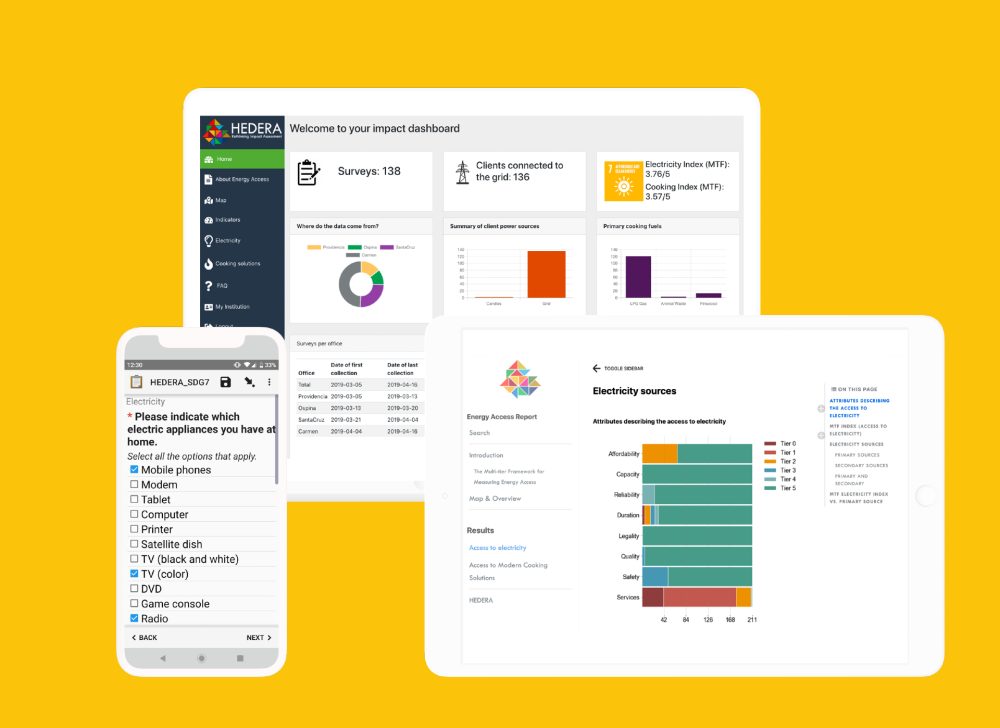

However, gauging the impact of microfinance is notoriously difficult. A multitude of microfinance institutions now provide the service, but in many cases there is little effort or ability to track improvements to the welfare or standard of living of recipients. That’s where Hedera Sustainable Solutions, a Berlin-based company, comes in. Their mission is to track the progress of microfinance efforts, to provide better services to clients and monitor contributions to the United Nations’ Sustainable Development Goals.

To achieve this, Hedera has developed a suite of digital tools which can be used to support microfinance institutions and NGOs in the field. Developed as the HEDERA Impact Toolkit (HIP), many of these tools work with already established monitoring frameworks, such as the World Bank’s ESMAP Multi-Tier Framework for access to energy and the WHO/UNICEF WASH service ladder, which monitors access to water and sanitation. Hedera collects and optimises impact data into easy-to-use and expedient tools, reducing training time and cost. This information can then be automatically collated and visualised on the Hedera platform, aiding communication between investors and investees, among others.

For example, Hedera’s Energy Access survey examines how families generate power, what this electricity is used on, their access to lighting and the frequency of accidents or health issues resulting from poor access to power. The results of these surveys can then be pooled into digital reports to inform more precise and impactful microfinance payments, monitor the progress out of poverty of payment recipients as well as support the SDGs.

Hedera also works with local institutions, companies and NGOs in the field to provide research support, training and the digital tools needed to efficiently analyse data. For example, in the Democratic Republic of Congo, Hedera has worked with the Appui-conseils aux Projets et Initiatives du Développement Endogène (APIDE) to visualise budget-related data, making it more transparent and more effective on the ground. Meanwhile in Colombia, Hedera has collaborated with the Rejuvenating Pueblo Viejo initiative which aims to promote sustainability education among children and adolescents, and give them a voice within local civil society. The Hedera Toolkit has been used to assess local needs and monitor progress over time.

The Microfinance Debate

Microfinance is not entirely without controversy. There is extensive debate over the effectiveness of micro-loans for alleviating poverty, and even the ethical implications of offering any kind of credit to near impoverished households. Hedera accepts microfinance does not necessarily end poverty, but can provide access to important services.

Supporters claim microfinance and microcredit provide a boost to households living on the border between poverty and self-sufficiency. Households who qualify for microfinance may be living on as little as 1.25 USD a day. This may cover basic food costs, but provide little income for anything else. Meanwhile, a medical emergency or other expensive unforeseen crises may cause a household to plummet into deeper poverty.

However, a simple loan of around 100 USD may be enough to push that household into a higher socio-economic bracket, provide security and allow for local entrepreneurism. Once basic needs are stabilised, microcredit recipients can devote time and energy to other endeavours, theoretically creating more productivity and boosting the local economy. Supporters of microfinance also suggest small loans often particularly benefit women by providing access to education as well as financial independence and additional opportunities.

But there are also criticisms of microfinance. Microfinance providers often make a large number of low value, high risk loans. With no guarantee of repayment, high interest rates — sometimes as high as 30 percent — are required. This likely limits the beneficial impact of the money and may further increase recipients’ financial problems. It is not unusual for microfinance recipients to take additional loans to make repayments on previous loans. The sheer number of microfinance institutions, many of which rapidly emerged in the 1990s, also means professionalism and transparency may be lacking. On some occasions, microfinance indebtedness has led to tragedy, with the BBC reporting a wave of suicides in India linked to microfinance loans.

Others suggest promoting entrepreneurship in small communities without the necessary commercial base is also of limited value, resulting in an over-saturation of certain products and cut-throat competition. Furthermore, although loans are often taken in women’s names, it does not guarantee they have control over those funds or they are invested into their well-being.

Much of these issues originate from a lack of transparency within the microfinance sector, as well as a lack of information about the immediate needs of communities and households. Projects like Hedera, therefore, may provide useful and actionable insights into the sector, mitigating some of the potential downsides of microfinance loans.